Key Insights into Senior Living Consumer Confidence and Sentiment

Share

To help providers prepare for the post-pandemic economy, occupancy data and trends from the National Investment Center for Seniors Housing & Care (NIC) was tracked, analyzed, and combined with Attane’s consumer confidence and sentiment survey. After aggregating a year’s worth of Benchmark data and insight into the mindsets and values of consumers, a clearer picture of the state of senior housing has emerged.

In April 2020, Attane kicked off a longitudinal study to track consumer sentiment and confidence in senior living during the COVID-19 crisis. Over time, and through six separate surveys, we compiled the sentiments of 250+ consumers. Throughout each respective wave, we surveyed the country to assess the current attitudes, beliefs and sentiments toward senior housing.

Let’s explore insights from this expansive collection of data and its implications for senior housing.

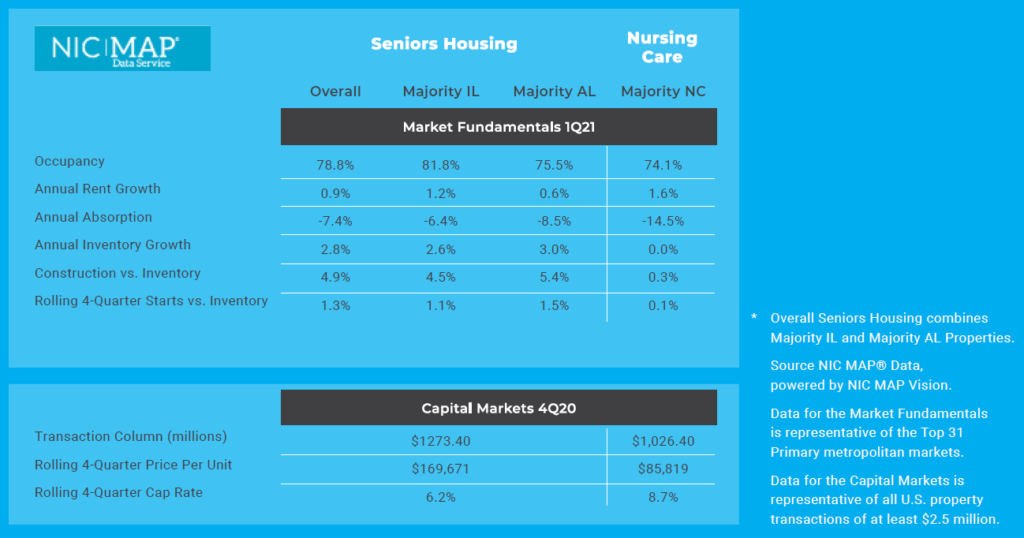

NIC Senior Housing Quarterly Analysis Q1 2021

The topline data and trends for lead volume and occupancy escalation are telling the story of an uneven year across senior living levels of care, with a long road to recovery. It’s also worth mentioning that occupancy levels are beginning to stabilize. While occupancy isn’t where it was prior to the pandemic, tailwinds are developing.

The breakdown of each level of care from the latest NIC data, combined with analyst predictions, gives us a sense of what the industry is collectively facing. That said, renewed optimism in senior living is beginning.

Industry Sentiment Is Shifting, and Rebounds Are Occurring

Renewed optimism in terms of senior housing occupancy and the overall market outlook stems from several areas:

Vaccine distribution

Increased lead volume

Move-ins accelerating across service lines

The following findings provide important at-a-glance insight:

Executives reported 90% of residents are vaccinated

65% of staff members at senior living communities are also vaccinated (and growing)

89% of executives across the industry have measured increases in lead volume every week since the beginning of 2021

74% of executives report lead volume has increased, but still hasn’t returned to pre-pandemic levels

While there’s room for growth, the statistics above point to a healthy rebound for senior housing. Subsequently, this shows prospects that the health and safety of residents and staff are a priority, which solidifies senior living as a trusted and safe place to live, especially in a post-pandemic economy and landscape.

Consumer Sentiment, Confidence and Trust in Senior Living — Waves 1-6

From the stringent and consistent analysis from waves 1-6 of the benchmark data, three primary takeaways have become evident.

3 Important Takeaways from the Consumer Confidence and Sentiment Survey

Consumer confidence and positive sentiment continue to rise — Consumer confidence does sit at lower levels than before the pandemic. During wave 1, consumer confidence regarding the safety of living in an IL community during a health crisis like COVID-19 sat at 22%. By wave 6, consumer confidence grew to 43%, a 21% increase. For AL/MC consumers, the same question was posed. During wave 1, consumer confidence fell to 20%. When asked again in wave 6, consumer confidence grew to 37%, a 17% year-over-year increase. This steady improvement from waves 1-6 shows the public considers senior housing a viable alternative compared to living at home, which is a positive outlook.

Significantly fewer people report they are “less likely to move to a senior living community now vs. pre-COVID” — This particular line of questioning was to understand “Are people more likely, less likely or just as likely to move into a senior living community?” The results indicate more people are considering senior housing now than in the past year, demonstrating seniors are less apprehensive to move into a senior living community.

Seniors 75+ are more confident and positive about senior living than other age segments — Seniors are more confident than they previously were about moving into a community. Prior to April 2020, seniors were the most apprehensive about considering a move into a community setting. With seniors 75+ leading the charge with improved confidence about living in a senior living community, it’s a positive shift into the mindset and perception of this key segment for providers.

In addition to the quantitative takeaways from waves 1-6, additional qualitative consumer trends have been gleaned after discussions with senior living leads.

4 Qualitative Consumer Trends

We listened to 500+ senior living leads over the last 180 days via focus groups and group discussions. The following trends represent the collective feedback from those conversations.

Challenges exist in staying at home — During the pandemic, people who chose to stay at home have experienced inherent and unexpected challenges not anticipated. For example, there are uncertainties regarding safety precautions with caregivers, issues with increased isolation, and an overall lack of social interaction. Additionally, issues of accessibility to care and the rising cost of home health care have also been expressed.

A “wait and see” mentality persists — Despite the positive headlines of vaccine distribution, many leads, prospects and depositors are still choosing to wait to move into a senior living community. Much of this sentiment has been contingent upon the availability of vaccines and waiting to see more stable herd immunity. We expect this trend to lessen as more adults become vaccinated and as infections decrease.

Couples are deciding to stay at home — During social isolation and enforced lockdowns, many of the seniors surveyed who are in a relationship have decided to remain at home. Couples appear to be delaying the move-in decision to later dates due to the social connectedness found at home.

Singles are more likely to accelerate the move-in decision — Seniors who live alone are yearning for socialization opportunities. The single individuals surveyed have indicated that despite the U.S. not reaching herd immunity, they’re more likely to consider moving into a community than cohorts in a relationship. The following quote sums up this mentality: “Limited social interaction is better than none.” Singles are more likely to plan a move to a community than initially planned due to the motivation of not being alone.

Need More Trends and Data? Watch the On-Demand Recording

The data and trends shared above depict a year of progress, but relentless focus to meet occupancy goals is still required. To actualize your goals, you’ll require a partner with the vital data and insights that are necessary to help your community succeed.

Watch the on-demand recording to gain additional context about the benchmark data from our consumer sentiment, trust and confidence surveys, and how your community can utilize it to accomplish your respective goals.

You May Also Like

Marketing to Seniors,Search Engine Optimization,Senior Living

What Senior Living Communities Need to Know About Google and Bing’s AI Changes

Marketing to Seniors,Paid Media/PPC,Senior Living

How AI Search Affects Paid Marketing

Marketing to Seniors,Senior Living

How AI Will Change the Customer Journey

Request A Demo

Get a closer look at how we can help you engage with success.